If you’ve been following Paradise Real Estate over the years, or are a past client, you may have noticed some changes to our company in the past 5 years. In 2017 the original owner of Paradise Real Estate, Dan Spano, asked another local agent to join up with him. That…

Paradise Real Estate

39 posts

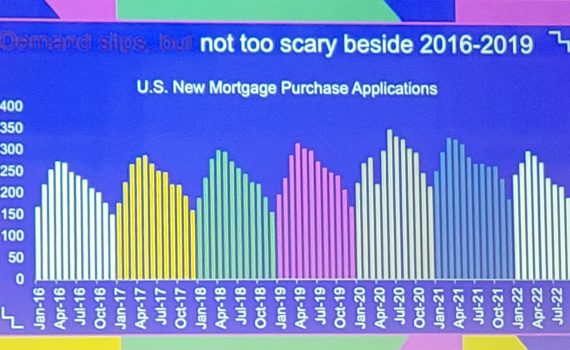

The following article is provided by the California Association of Realtors from their fall business meetings. Images are screen shots our team personally took when we attended the economic market forecast luncheon that went into detail on the California real estate market forecast. For local Tahoe real estate market data,…

2902 Oakland AvenueSouth Lake Tahoe, CA 96150 Listed at $538,238 Old Tahoe charm with a modern twist! This cute 2 bedroom cozy Tahoe cabin is situated in the prime South Tahoe neighborhood of Al Tahoe, with locals favorite beaches located just down the street and trails in the meadow just…

As time goes on, and the seasons change, our Lake Tahoe real estate market has gone through some big changes. The whole housing market is a different place that is was just 1 year ago. There are new issues, rules, and opportunities. So what exactly has changed? How does the…

People have been coming to Tahoe since the early 1900’s. It is a truly unique vacation destination and recreation paradise. But did you know that it is also a wonderful place for families? Whether you are bringing your little ones here on vacation, or looking to move here full time,…

Drones Changing The Real Estate Marketing In the Lake Tahoe Real estate market most of my clients “shop online” for their next potential home. Viewing a drone video of the property they are interested in will help get a better feel for the property. Therefore Lake Tahoe home buyers are…

There is a good reason that over 3 MILLION people visit Lake Tahoe every year. From skiing fresh powder to laying on beautiful sand covered beaches, sometimes on the same day, Tahoe has it all! It doesn’t matter what your age, there is something for everyone. Hiking, beaches, boating, and…

As I recently wrote, the biggest decision you need to make when buying a home in Lake Tahoe is selecting your Realtor. However, before you get that far into the process you may want to just browse and get a feel for the Lake Tahoe real estate market. Nowadays, many potential…

I am pleased to announce some really big changes for Paradise Real Estate of Lake Tahoe! This has been such a fabulous year that we’ve found the need to expand and provide a deluxe Lake Tahoe real estate showroom! Home buyers will be able to enjoy an interactive search tool…

Even though the official start of construction doesn’t begin until May 2015 on the new Edgewood Tahoe Resort, the golf course is already undergoing major changes to prepare for the big project. The 8th and 9th holes have been altered for golf this fall, and then they’ll be reconfigured prior…

There are important tasks that homeowners in Lake Tahoe should complete before winter each year. It’d be nice if we could look into a crystal ball and see if a mild winter or a heavy snow winter is going to hit the region, but we can’t so we just need…

This is the third part in our series on building a dream home in Lake Tahoe. We’re following builder Peter Stromberg and going through the same steps he is taking, from inception to completion. I’ll be sharing pictures, tips and pointers so you can see what is involved and the…